Travelzoo (TZOO) Valuation

Travelzoo (TZOO) is an old-school online travel company that makes money primarily through distribution of travel deals via email newsletters.

Travel suppliers (i.e. Air France, Royal Caribbean, Hilton Hotels & Resorts) pay listing fees to get exposure to the newsletter audience and it is a particularly good way for companies to sell excess inventory (i.e hotel rooms, airline seats, etc). This inventory generally has a fixed cost, so it makes sense for companies to sell it at a discount if it would otherwise remain unfulfilled (if you have empty seats on a flight, and you are going to fly the plane anyway, the costs of selling those remaining seats are very little).

One of TZOO's key value propositions to advertisers is its scale. The newsletters reach 30MM+ subscribers, the website has ~10MM unique visitors / month (likely large overlap with email subscribers clicking through on deal links), and the mobile apps have been downloaded 6.6MM+ times. In general, the larger the audience, the greater the pricing power TZOO has with advertisers.

Growth Prospects

TZOO is not an exciting growth story. The technology and distribution model seem antiquated, and the website looks like it was last designed in 1998. On the face of it, the company is so unexciting that it took me a long time to dig into it, despite multiple recommendations from a good friend.

Geographically, 61% of revenue is generated in North America, 33% in Europe and 6% in Asia. Asia was once heralded as a major growth prospect, but mounting losses caused them to recently pull out of the market.

For the remaining markets (North America and Europe), newsletter subscribers have been relatively flat; they are spending money mainly to tread water. App downloads have fared modestly better, but it is unclear how much of this is incremental to existing email members, and how much revenue the app generates.

There have been efforts to diversify revenue streams. Up until early 2017, TZOO offered two travel search engines (SuperSearch and Fly.com), which were "discontinued to focus on the Travelzoo brand." TZOO also currently offers Local Deals (i.e. a coupon / voucher for a restaurant), but this segment only accounted for ~14% of revenue in 2019, and has been on a steady decline for the past 8 years.

More recently, they acquired 60% control of Jack's Flight Club (JFC) for $12MM, with an option to acquire the remaining portion by the end of the year. JFC is an email newsletter that helps users find cheap flight deals, and operates on a freemium model with additional benefits for paid members. It currently has 126k premium subscribers.

Hidden Value

Despite lackluster growth, the core business (email newsletter travel deals) is solid. Membership and revenue have held steady over the past few years.

Operating margins have also been strong, but they have been masked by poor performance in the Asia segment:

Excluding Asia, operating margins over the past 3 years have been ~14%, vs a reported ~4%. Since the Asia business is being discontinued, this headwind will recede. Tax rates are also being distorted by the Asia business, since losses aren't being used to offset North American and European income.

While modest, mobile app download growth has also been promising. Email lead generation is unlikely to go away, but the mobile app gives them more optionality in distribution. It also gives them the ability to push richer, more relevant content to their user base. The app is favorably reviewed (4.9 / 5 rating on Apple's App Store, with 61k reviews), but again it is unclear how these metrics translate into revenue.

The JFC acquisition could add real value, and the fact that it is heavily aligned with their core business (email marketing) is promising. "At the time of the acquisition, the immediate contribution to Travelzoo’s financial performance was an additional 5% revenue growth and an additional EPS of $0.20 for 2020" (source), which implies that they expect it to generate ~5MM in revenue and 2.4MM in net income for 2020, even without additional cross-selling to their existing, large Travelzoo membership base.

There is a full valuation below, but essentially you have a business that has the potential to generate ~$19MM in operating income trading at an enterprise value of ~33MM (based on March 27, 2020 share price of $3.57, and adjusting for the JFC acquisition), which appears remarkably cheap.

Another Wrinkle

TZOO's share price has seen an large decline (-37%) since March 12, 2020 - far more than the decline of the S&P index, Russell 2000 micro-cap index, and comparable travel stocks:

On March 17, 2020 TZOO's share price declined 20%, while the S&P index fell 6%. On the same day, 94k shares of TZOO were sold by Azzurro Capital Inc. This was nearly 50% of total volume traded that day.

The footnotes to the SEC filing indicate that this sale was "involuntary" and sold by E*TRADE Securities LLC.

Azzurro Capital Inc. is ultimately controlled by Ralph Bartel, founder of Travelzoo and current director of the company. Azzurro Capital currently owns ~42% of TZOO's outstanding shares.

There are many other days from March 12, 2020 to March 25, 2020 (a historic period of general market volatility) where this "involuntary" selling pattern from Azzurro Capital repeats. It is left to the reader to speculate why these sales might have been involuntary, but it is not hard to imagine why it might have magnified TZOO's share price decline.

Risks

Coronavirus

The obvious risk here is the Coronavirus, which has essentially shutdown businesses around the world. The travel industry has been particularly hard hit - a large portion of the world population is in quarantine, countries are closing off their borders, and airlines and hotels are at risk of going bankrupt.

It's hard to make money serving up travel deals if all of your suppliers go out of business and if none of your customers can leave their homes.

Liquidity

TZOO appears to run with a fairly lean balance sheet. This was probably optimal in normal times, but they may have little cash left to weather the Coronavirus storm after factoring in the $12MM acquisition of JFC. If, as seems likely, they do not generate much revenue for the next few months, they may face serious issues with liquidity. Rough guesses:

Millions USD Note 36 Current Assets end of Q4 2019 (35) Current Liabilities end of Q4 2019 (12) Jack's Flight Club Acquisition in Q1 2020 2.5 Estimated cash from operations Q1 2020 -8.5 Estimated liquidity end of Q1 2020

Which doesn't look great. However, a large chunk of current liabilities ($13.7MM) are "merchant payables." When a customer buys a Local Deals or Getaway voucher from TZOO, they pay TZOO directly. TZOO then pays the "merchant", after taking a cut. It is unclear exactly when TZOO pays the merchant. Groupon appears to pay 33% immediately, 33% after 30 days, and 33% after 60 days. On the other hand, Groupon also says that it "will have no obligation to advance amounts that have been paid to Groupon by a purchaser until Merchant has complied with Merchant’s obligations under this Agreement", so there appears to be some flexibility in payment terms.

TZOO is trying to extend voucher expiration dates and offering "promo credits" for future use. This will likely help extend the runway for merchant payables and reduce cash outflows. They have a refund reserve for the worst case scenario, but it likely won't be enough. Making a few other, very rough, assumptions:

Millions USD Note -8.5 Estimated liquidity end of Q1 2020 7 Measures to delay "merchant payables" (2) Increase in refund reserves -3.5 Estimated liquidity end of Q1 2020

Expenses

Looking at expenses going forward:

Operating expenses in 2019 were $90MM.

The recently passed US stimulus bill may provide significant relief in terms of payroll and rent support. They have 418 employees with a median salary of $60k; the average salary is likely greater than the median, due to outsized executive pay, so we can assume payroll is at least $25MM.

Only employees who live in the USA appear to be covered by the stimulus bill. According to TZOO's "revenue per employee" disclosures, this works out to ~188 employees in North America, which would imply actual payroll relief on the order of $11MM.

They have offices around the world, but the largest expenses are likely for their offices in NYC. Assume another $3MM in rent relief from the stimulus bill.

$10MM of expenses consisted of online advertising, which can likely be paused quickly.

Putting everything together:

Millions USD Note 90 Baseline operating expenses from 2019 (11) US Stimulus Bill payroll relief (3) US Stimulus Bill rent relief (10) Pause all online advertising (8) Cut / furlough 33% of workforce 58 Annual fixed opex 5 Monthly fixed opex

Cash Flow

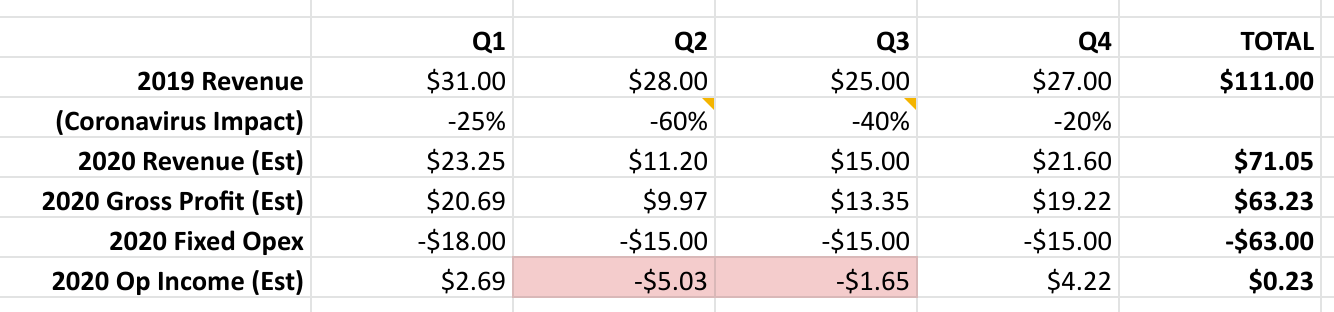

While there is a lot of pessimism and uncertainty about the economic recovery, especially as it relates to travel, China offers a clue. Quarantines lasted around 3 months. At the bottom, air travel demand was 15% of normal, but is now back to 30% of normal. Domestic travel is picking up.

TZOO can focus more on local deals and staycations - for example, restaurants and hotel stays within driving distance, so the impact should be less dramatic than the decline in China air travel.

Using 2019 quarterly revenue as a baseline, adjusting for Coronavirus impacts, and factoring in reduced operating expenses outlined above:

Adding everything up - and again, this is super rough - they might need $10MM+ (3.5MM in near term obligations, 6.5MM to cover Q2/Q3 2020) of liquidity to weather the downturn.

Funding Sources

They have a long record of profitability and cash flow (especially if you exclude their discontinued Asia business). Their core business is simple and predictable. Unless you assume that people will never travel again, it is hard to imagine they won't be able to receive a traditional bank loan, stimulus backed bank loan, or equity infusion to bridge the next few months.

Worst case, the majority owner (Azzurro Capital) and founder, Ralph Bartel, appears to have significant assets, and might be able to personally guarantee any loan with sufficient collateral. He has previously loaned money to Travelzoo and its subsidiaries. It seems unlikely that he would let a cash cow like TZOO die from what is a serious, but likely temporary, issue.

Finally, these worst case scenarios assume that revenue will fall inline with travel supplier trends in China. But even if people are unable to travel during the next 3-months, they may still be interested in purchasing (and prepaying) for travel that occurs in 6-12+ months, when the threat from the virus is likely to be reduced. In fact, TZOO is already advertising refundable deals for travel windows far in the future. This might help generate near-term revenue and cash flow - even if people aren't necessarily traveling yet.

Management

TZOO's largest shareholders are Ralph and Holger Bartel, brothers who own roughly 42% and 5% of shares respectively. Interestingly, the recent March sales from Azzurro Capital may have put their combined ownership below the 50% threshold for majority control.

It is unclear how committed they are to enhancing shareholder value. The main avenue by which wealth has been returned to common shareholders has been through aggressive buybacks over the past 10 years, with outstanding shares having been reduced by nearly 30%.

But that hasn't resulted in any noticeable stock appreciation (though, to be fair, most of this decline has been in the past month):

Some of these share purchases have been negotiated directly with Azzurro Capital and Holger Bartel, but this appears to be a relatively small proportion compared to open market purchases. In the past 3 years, the board has authorized the repurchase of ~2.5MM shares, roughly 20% of shares outstanding.

It is unclear what the capital allocation end goal is here - but at these share prices, under normalized earnings power for the core businesses, TZOO would generate a ~20% free cash flow yield, which could be used for huge buybacks or large dividends. And if the Bartel's no longer have control, then TZOO might become a very attractive acquisition target for a private equity firm or travel company on more solid financial footing.

Valuation

There are a lot of moving parts, uncertain assumptions, and very back-of-the-envelope type calculations outlined above. But, simplifying a bit, the investment opportunity hinges on only two key factors:

How long and to what degree will the Coronavirus depress travel?

Will TZOO have enough liquidity to survive this depression?

My baseline valuation includes the following assumptions, which I believe are fairly conservative:

Near term Coronavirus hits outlined above, followed by a gradual recovery in 2021 - 2022

$10MM in debt / equity to fund near term liquidity concerns

Flat growth thereafter, accelerating into terminal revenue decline of -5%

13% operating margins, inline with historical norms

Roughly $5MM / year in incremental revenue from JFC and $4MM in operating income.

https://docs.google.com/spreadsheets/d/19TkHZkNt-lwLp6YY8e1YDjzAme_Au0aRv5wD_eN0kto/edit?usp=sharing

TZOO is currently trading at $3.57. Using the assumptions above, it's worth roughly $5.

Using more pessimistic assumptions, and assuming they have to take on $20MM in funding, it's worth $4.12.

Using more optimistic assumptions, if you assume growth is flat (rather than -5%), and that JFC's outsized operating margins increase the long-term average of the company as a whole to 15%, it's worth $8.76.

Another way to look at TZOO's valuation is to just look at the asset value of their email list. They have 30MM members. Average cost per acquisition has ranged from $2-3. Even at the low end of the range ($2), an established company could acquire leads more cheaply by buying TZOO for $60MM than by marketing elsewhere. This would value the company's shares, on a simplified asset basis, at $5.13. These are famous last words - but it's hard to see the company, worst case, liquidating for less than that.

Disclosure: I am long TZOO.