Excess Savings

And a slight update in strategy

Let me preface this by saying that I am not a macro-economist and that everything below could be complete gibberish. But, intuitively, the following logic seems to make sense:

In the aggregate, households have “unprecedented levels of excess savings - defined as the difference between actual savings and the pre-recession trend,” driven by the pandemic and extraordinary government stimulus.

Estimates for when these excess savings will be depleted, like calls for a recession, have been repeatedly pushed back. Recently, they have been revised upwards from ~$400B to $1.2T, which may help explain the continued, unexpected strength of the economy.

Current strength in consumer spending is unsustainable relative to the long term trend. Consumers are spending more than they are earning, and drawing down their excess savings. Eventually these excess savings will run out.

Consumer spending accounts for ~70% of the US economy, so the effects of a return to a sustainable equilibrium that does not rely on an infinite supply of excess savings would be material:

The gap between real consumption and real disposable income has been financed by drawing down excess savings. If the U.S. saving rates had remained at the pre-pandemic average value (implying zero excess saving), the two indexes would have tracked in tandem. Real consumption would then be some 3 percent lower than at present for the given level of income. By itself, this would leave real GDP about 2 percent lower.

Weaker growth would be fine (from an investment standpoint) if it was reflected by cheaper valuations. Yet, by measures historically and most reliably correlated with long term returns, the S&P 500 is near its most over-valued level in history. The index has only been more expensive during the speculative height of the COVID bubble (remember NFTs?), and valuations still exceed the peaks of both the dotcom bubble and the eve of the Great Depression.

That’s not to say the market will crash tomorrow, or that it will crash at all. But if you believe consumer growth is unsustainably high, and that valuations are extreme, the odds of a long-term, positive outcome from blindly investing in the S&P 500 index seem extremely low at this time.

Portfolio Updates

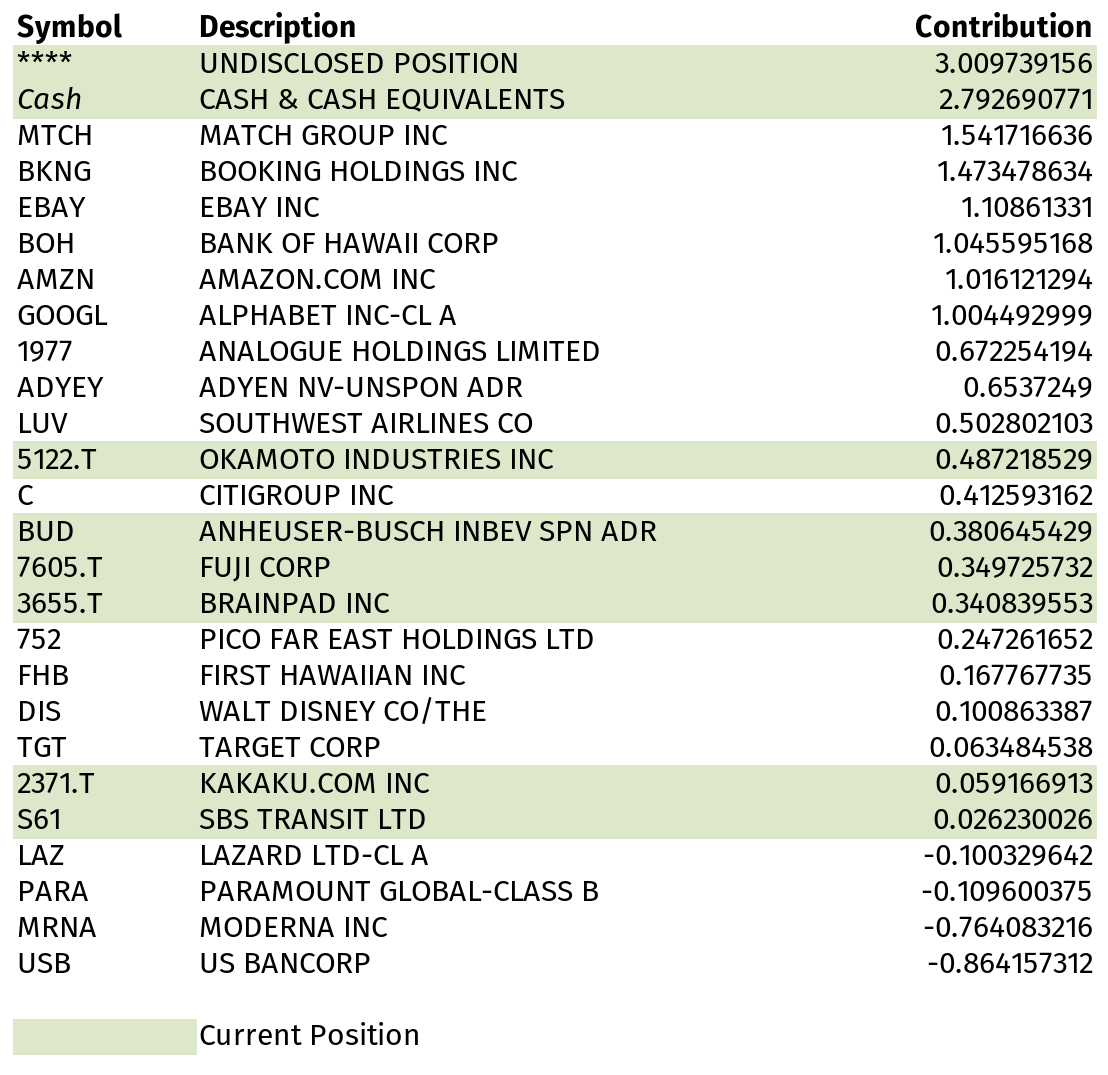

Despite my gloomy prognostications for the broader market, I’ve found pockets of value, for brief times, in some individual stocks. This is perhaps best illustrated by the contribution to total return of various positions held throughout the year:

The typical pattern has been that I become cautiously optimistic (and buy a handful of companies), but then my innate skepticism at broader market conditions causes me to sell all but my most certain positions.

Surprisingly, this “strategy” has been highly effective this year: overall performance has been ~16.7%1 vs 15% for the S&P 500 year to date, despite ~70% cash holdings on average throughout the year. A few things stand out:

Timing has been good. For example, both MTCH and LUV are down roughly 30% YTD, but I’ve managed to make money in them by buying and selling at the right times. Part of this is sticking to a strict valuation discipline (i.e. only buying at a large discount to estimates of fair value and selling when fair value is approached, regardless of holding period), but part of it is also luck.

Turnover has been higher than I’ve liked. Again, part of this is due to a strict valuation discipline (companies reaching fair value quickly), but part of it is also due to my lack of confidence in weaker companies in a highly uncertain macroeconomic environment, which results in frequent reassessments of value.

With the exception of a few stocks, I’ve managed to avoid too many big losers. Part of this is due to demanding a large margin of safety on any purchase, but part of it is also luck and timing.

I mention YTD performance because I want to emphasize that my bearish overall view isn’t driven by bitterness over having missed out on any stock market rallies this year, and also because I’ve reached a fundamental turning point in my perception of risk: namely, I believe economic conditions, psychological sentiment and general valuations are now so precarious, and that the outcomes are so weighted to the downside, that I am content to sit out all but the most obviously undervalued and certain positions.

I am currently holding 80% in cash while I await a more favorable environment, and will try to focus on ideas outside of the S&P 500, outside of the US, and more inline with special situations and opportunities uncorrelated with the general market. Even if I can only find a handful of attractive opportunities per year, I believe that results should be satisfactory relative to the alternative.

Again, this is not investment advice! History also shows that, long term, holding cash is not a great investment. Furthermore, this is merely a snapshot of my current thinking, written to personally clarify my thoughts and approach more than anything else, and my strategy could change at any time.

For some reason, the sum of individual “contributions” to total return doesn’t add up to the aggregate total return. The aggregate time-weighted return looks correct when double-checked via other calculations, but if anyone knows why this discrepancy appears in Interactive Brokers reports, please let me know!