Thoughts on Airlines; Southwest (LUV) Valuation

There are few industries with as much uncertainty right now as airlines. Even the "Oracle of Omaha", Warren Buffett, admitted that the future of airlines was too unclear for him and recently sold all of his positions. Buffett and many other intelligent people believe that the future of air travel has fundamentally and permanently changed, similar to how heightened security checks implemented after 9/11 still exist today. Although I am no expert, and readily admit that there is a large range of possible outcomes amidst great uncertainty, I believe that these fears are exaggerated given the current evidence, and that a handful of airlines represent attractive investment opportunities.

Common Fallacies

Similar to discussions of the coronavirus, debates about investing in airlines are highly polarizing. This seems to have resulted in a few common fallacies which I will attempt to dispel below. Again, I am no expert - just someone who is attempting to get a clear reading of the facts and making a bet that I think has a favorable expected return; feedback and countervailing opinions are welcome.

Claim #1: During the Great Financial Crisis (GFC), it took 7 years for air passenger numbers to recover.

This is a true statement, but misleading and largely irrelevant to the current situation.

During the GFC, total US passenger traffic peaked at 770MM in 2007 and didn't recover until 2014. However, even at the low (700MM passengers in 2009), this represented a decline of only 10%. In other words, even with all of the structural economic issues during an unprecedented, historic recession, air passenger traffic was still 90% of previous levels. This implies some baseline level of essential travel demand, even in dire economic situations.

What would happen if US air passenger numbers fell 10% to a new, lower baseline? They would simply be at 2016-2017 levels, a period during which airlines were still highly profitable. Even if the new baseline was -20%, they'd still be above 2012 levels, also a period during which most airlines were profitable.

Of course, we are currently talking about a -90% decline in air traffic, not a -10% decline. But it would be a mistake to assume that the recovery from -90% back to normal will be evenly spread across the next 7 years, even in the worst case. Instead, it seems more likely that the recovery will occur in two phases:

Temporary Shock (2020 - 2022) - Travel will be severely depressed for 1-2 years, until there are viable treatments or vaccines. The exact shape of this recovery is highly uncertain, but most medical experts agree that this time-frame for therapeutics and vaccines seems reasonable. Other factors, such as social distancing on planes, mandatory mask requirements, more robust testing, cheaper fares and human nature may help drive demand up modestly. Air travel recovers from 10% of previous levels to 70-80% of previous levels.

Structural Shock (2023 - 2027) - Once air travel recovers to the new baseline, it might take an additional 4-5 years to recover from the effects of a structurally weakened economy. Air travel slowly recovers from 70-80% of 2019 levels to 100%, similar to the GFC.

This may seem overly optimistic, but history has also shown that air travel recovers quickly from similar pandemics, and that life can return to normal.

Claim #2: Travel and societal norms will be forever changed

I hear this claim a lot, and have written about it before. I still believe that the base case, from all historical evidence, points to the fact that humans will be eager to return to "normal normal", not a "new normal", as soon as possible. This will depend on how quickly people can feel safe and comfortable around other people. Nobody knows precisely when that will be - but I am willing to bet that it won't be "forever", and that public space, and thousands of years of human nature, will not be "permanently reconfigured."

The 1918 pandemic killed 50MM people, yet that did not cause a permanent shift in human behavior. The 1958 pandemic killed 1.1MM people and the 1968 pandemic killed 1MM people, yet hardly anybody talked about them until recently, and even now they seem like curious footnotes in history.

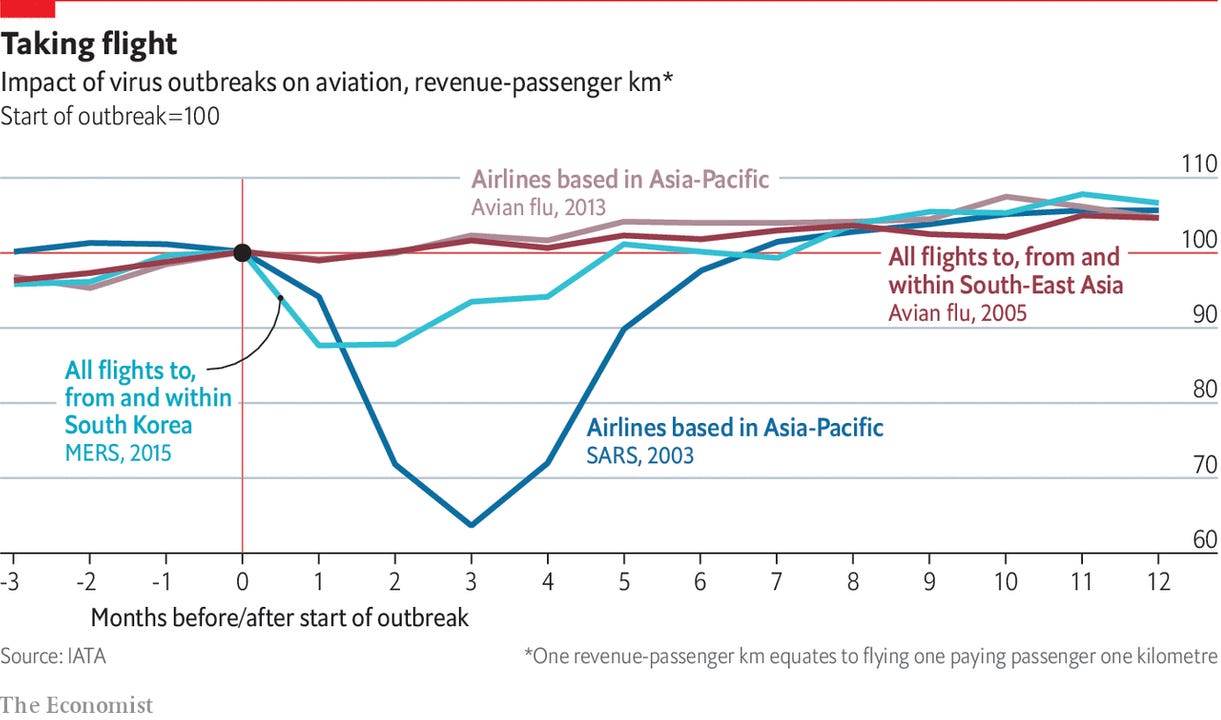

We can also see what happened to air travel during previous, more recent pandemics:

Once the outbreaks were contained, travel rebounded quickly. SARS and MERS affected far fewer people, but were also far more deadly.

Another, more contemporaneous data point comes from scheduled domestic flights in China:

The recovery seems modest, but it's also important to keep in mind that this outbreak has only been going on for a few months, despite "quarantine time" seeming to stretch into eternity.

According to The Harris Poll, 50% of people claim they will fly on a plane within the 6 months, and 64% within the next year. Among people under age 65, who account for roughly 83% of travel spend, and for whom the risk of death is far lower, the proportion is slightly higher. These aren't fantastic numbers, and who knows what people will actually do; but they are inline with China flight numbers, and they also aren't zero.

Overall, although it's easy to believe it's the end of the world, the base rate argues for a more optimistic view.

Claim #3: Airlines are burning through $x / day and are doomed to bankruptcy

Most airlines are burning through large amounts of cash per day, and some will almost certainly go bankrupt. Southwest Airlines, for example, estimates that it will burn through $30-35MM / day in Q2 2020.

This sounds frightening, but must be placed in the proper perspective. First, Southwest has ~$16B in liquidity. Even at these burn rates, it has 16 months of cash remaining.

Furthermore, 16 months is likely the worst case scenario, and their runway realistically extends for much longer. On the revenue side, they are assuming 5% load factors, and a 90-95% drop in revenue, for both April and May. Even modest improvements in demand, which seem likely once stay-at-home orders are lifted, will reduce cash burn. Life should improve after Q2.

On the cost side, nearly 50% of their expenses comes from payroll. As part of the CARES act grant, they will not be able to materially reduce payroll expenses until after Sept 30th. But if demand doesn't return by then (as seems likely), layoffs / furloughs are inevitable, and their costs will come down, further reducing cash burn.

There is no question that airlines are in a tough situation. But most of them have a long runway to make adjustments, and this gives them a lot more flexibility than in previous crises. Businesses are dynamic entities, and the pandemic is a situation in which the relevant facts seem to change daily; it would be a mistake to extrapolate worst case cash burns indefinitely into the future.

Claim #4: All airlines are the same and will have similar outcomes

One puzzling aspect of Warren Buffett's decision to sell all of his airline holdings is the implication, frequently touted, that all airlines are equally poor investments.

Southwest Airlines owns most of its planes (as opposed to leasing them) and has a much lower cost structure and a much longer cash runway than American Airlines, United or Delta. Almost all of its flights are domestic, exposing it to far less risk and uncertainty than the other carriers, which have a high proportion of international travel. It is also more focused on leisure travel, which historically has bounced back more quickly than business travel.

Even the intuitive assumption that a downturn in passenger traffic will apply equally to all carriers is faulty. Low cost carriers actually grew their traffic during the GFC, and Southwest reported 47 consecutive years of profitability before this one.

Claim #5: There are too many planes

This is an interesting claim and I only bring it up because it was mentioned by Buffett multiple times as one of the reasons he sold. Specifically, he believes that if long term demand falls 20-30%, you'll still have the same number of planes, leading to oversupply and reduced profitability.

This may be true in the very short term, but will be balanced by a few factors. First, airlines are already taking the step of retiring older planes more quickly. Second, airlines are delaying and cancelling orders of new planes. Aircraft delays, previously a source of frustration, turned out to be beneficial; the pain of oversupply will likely be most acutely felt by Boeing and Airbus.

Another interesting twist is that most airlines are now blocking out the middle seat to enforce social distancing on planes. Roughly, we can estimate that this will reduce capacity by 33%. If this is the "new normal" until people feel comfortable flying in more crowded conditions again, then, unintuitively, airlines might not have enough capacity, even with a 20-30% reduction in demand. Some might argue that these load factors are economically unsustainable, but there are many other factors (price (in)elasticity of air travel, fare increases, record low oil prices, etc) that make this a less than foregone conclusion.

Southwest (LUV) Valuation

A valuation of Southwest Airlines, using the general assumptions outlined above, can be found here:

https://docs.google.com/spreadsheets/d/13_1TOHIsXLn0TRRcodPL_ufvPFZf7xRYXn1Z1ytO1qs/edit

The model assumes that air travel will remain heavily depressed for the remainder of the year, with revenue falling -75% YoY. A modest recovery is assumed over the next few years, but even then Southwest exits 2022 with revenue <80% of 2019 levels. It takes an additional 4 years (2026) for LUV to reach 2019 levels again.

Again, I would caution that there is great near-term uncertainty in the particular shape of the recovery. There could be a second, more devastating wave of illness in the fall. Conversely, a promising therapeutic could arrive more quickly than anticipated. Despite this near-term uncertainty, I believe that the situation will have dramatically improved after two years, and that Southwest has the liquidity and adaptability to weather even an extremely pessimistic scenario in the interim.

Finally, I make the key assumption that there hasn't been a permanent change to demand in the long term growth trajectory of travel. Based on the historical facts, and my personal assessment of human nature, this seems like the most likely outcome. If you believe, like Buffett, that the fundamentals of the business are permanently altered, then airlines may not be worth the risk.

Disclosure: I am long LUV